QUICK ANSWER

What do dropping mortgage rates mean for Tampa Bay buyers and sellers in 2026?

The 30-year fixed mortgage rate dropped to 5.87% as of February 2026 (Zillow), the lowest since September 2022. Tampa Bay’s housing market is shifting toward balance with approximately 4 to 5.4 months of supply, giving buyers more negotiating power while sellers benefit from improving demand as affordability gets better. Population projections show the Tampa Bay region adding roughly 397,000 new residents by 2030.

What’s in This Guide ▾

KEY TAKEAWAYS

- 30-year fixed rate at 5.87% — lowest in 3+ years, down from 6.85% one year ago

- A buyer saves $277/month on a $420K home compared to 7%, or $3,324/year

- Tampa Bay inventory at 4 to 5.4 months of supply — healthiest since pre-pandemic

- Buyers have real negotiating power: seller credits, repairs, and rate buydowns are back

- Sellers who price to current comps still see strong first-week activity

- Tampa Bay projected to add ~397,000 new residents by 2030 — structural demand intact

- This is not 2008: median credit scores ~748, homeowner equity exceeds $17.5 trillion

JUMP TO

- Where Mortgage Rates Sit Right Now

- Why a 1% Rate Drop Changes Everything

- What’s Happening in Tampa Bay’s Market

- This Is Not 2008. Not Even Close.

- What I’m Seeing From My Desk

- Why Buyers Should Be Acting Now

- Why Sellers Should Be Encouraged

- The Bigger Economic Picture

- The Long-Term Case for Tampa Bay

- The Insurance Factor

- Rate Forecasts

- The Refinance Opportunity

- Frequently Asked Questions

Updated February 23, 2026

The Story Nobody’s Telling You

Right now, mortgage rates are lower than they’ve been in over three years. Buyers are getting pre-approved again. Sellers who price correctly are seeing real activity in the first week. And most people are still sitting on the sidelines because they’re reading headlines from six months ago.

I work Tampa Bay real estate every day. Seven counties, from Pinellas to Polk, Citrus to Sarasota. And what I’m seeing on the ground doesn’t match the doom scrolling.

Here’s the actual situation, with actual numbers.

Where Mortgage Rates Sit Right Now

Let’s start with what matters most: the rate.

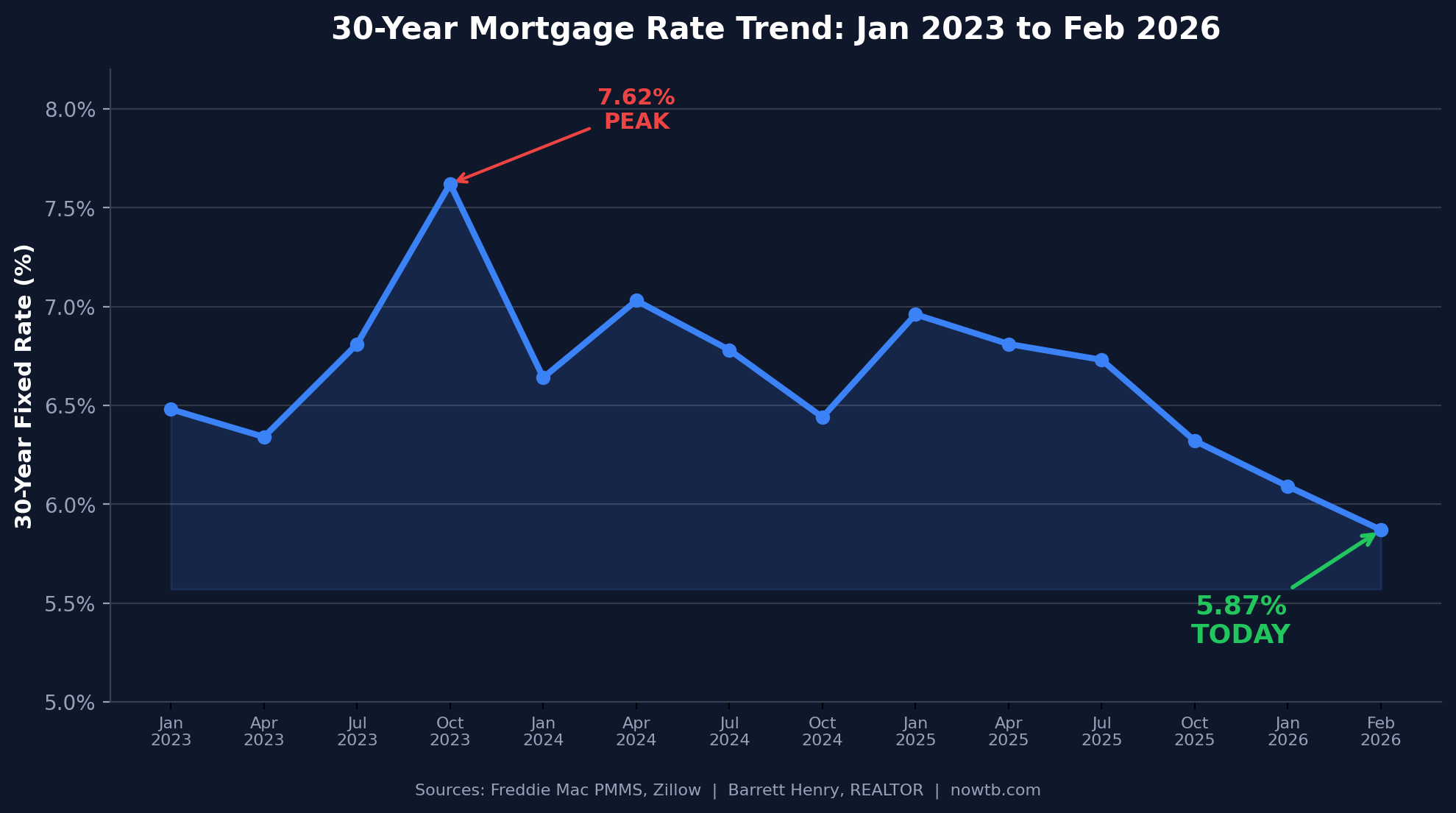

As of today, February 23, 2026, the average 30-year fixed purchase rate sits at 5.87% according to Zillow’s daily tracker. Freddie Mac’s weekly average came in at 6.01% as of February 19, which was the lowest weekly reading since September 2022. The 15-year fixed is even better at 5.35% (Freddie Mac) to 5.37% (Zillow).

To put that in context, one year ago the 30-year averaged 6.85%. That’s nearly a full point higher than where we are today.

And this isn’t a one-day blip. Rates have been trending down since late 2025, supported by declining inflation, a stabilizing job market, and the Federal Reserve’s three consecutive rate cuts at the end of last year. The Fed held steady in January 2026 and doesn’t meet again until mid-March.

Going forward, Fannie Mae projects the 30-year rate averaging near 6% through the end of 2026, possibly dipping toward 5.9% by year-end. The Mortgage Bankers Association expects rates around 6.10% through most of the year. Either way, we’re in the best rate environment since 2022, and some borrowers are already locking in rates in the mid-to-high 5s depending on credit profile and loan structure.

Why a 1% Rate Drop Changes Everything (In Dollars)

People don’t buy interest rates. They buy monthly payments.

So let’s do the math on a typical Tampa Bay purchase.

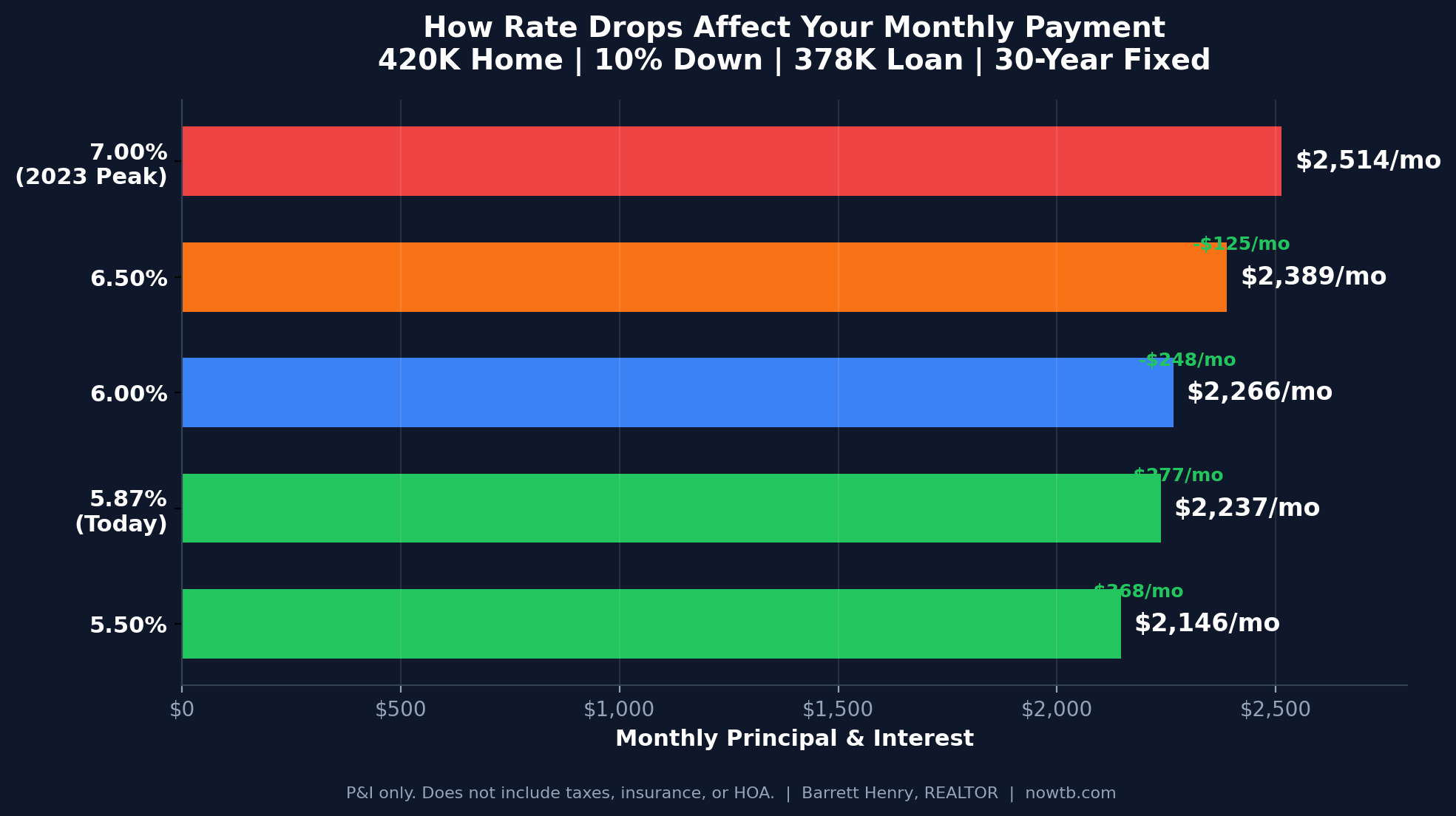

Scenario: $420,000 home. 10% down. $378,000 loan. 30-year fixed.

| Rate | Monthly P&I | Annual P&I | Savings vs 7% |

|---|---|---|---|

| 7.00% (2023 Peak) | $2,514 | $30,168 | — |

| 6.50% | $2,389 | $28,668 | -$1,500/yr |

| 6.00% | $2,266 | $27,192 | -$2,976/yr |

| 5.87% (Today) | $2,237 | $26,844 | -$3,324/yr |

| 5.50% | $2,146 | $25,752 | -$4,416/yr |

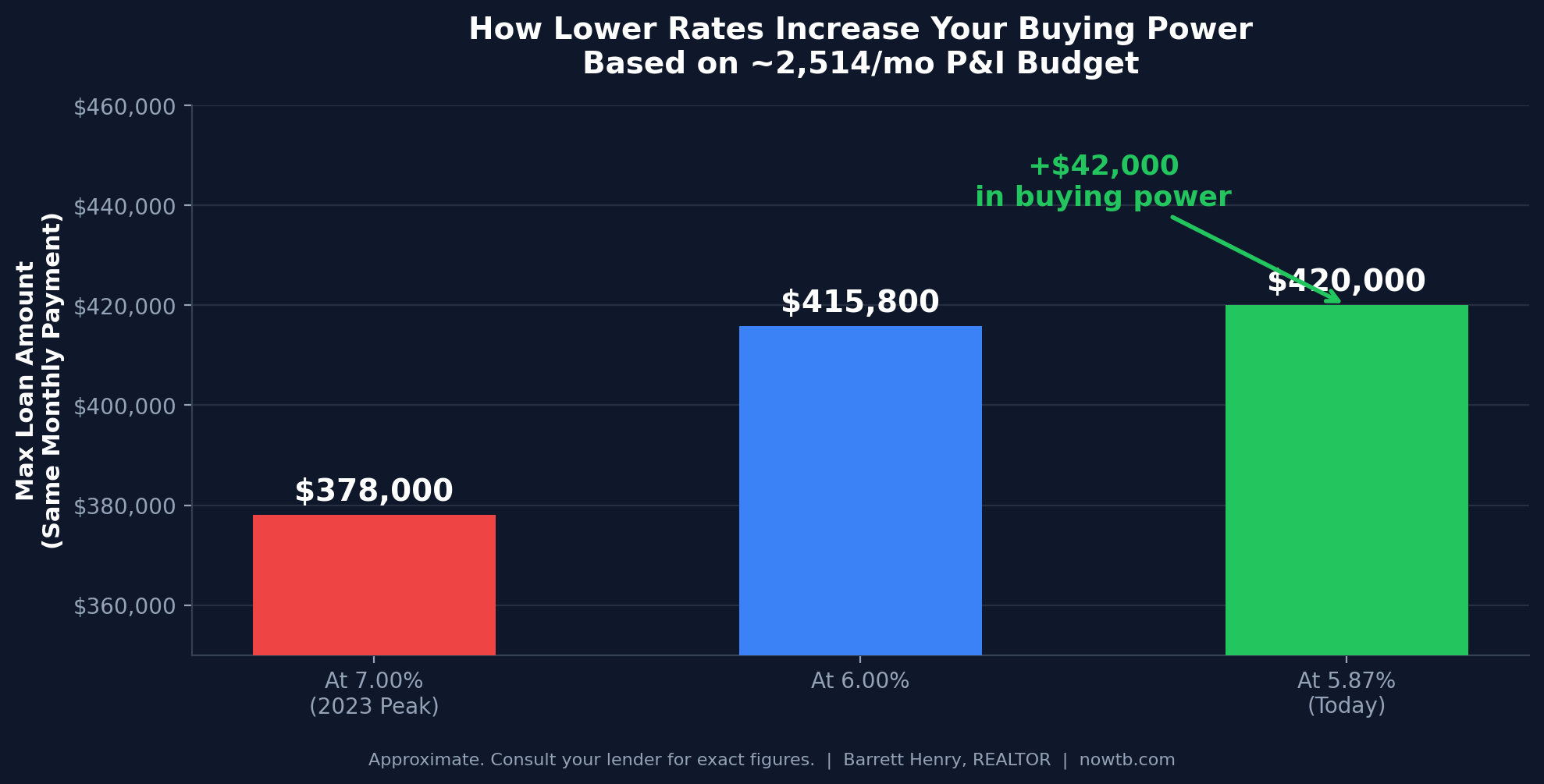

That $277/month difference between 7% and 5.87% is $3,324 a year. Over the life of the loan, the savings are massive. But more immediately, it means a buyer who couldn’t qualify at 7% might now qualify at 5.87%. It means a family that was stuck at $375K can now look at $420K.

Freddie Mac’s chief economist noted that purchase applications and refinance activity have jumped as rates have come down, and the spring sales season looks poised for stronger activity.

What’s Happening in Tampa Bay’s Market Right Now

National headlines don’t tell you what’s happening in Valrico or Riverview or South Tampa. So here’s the local picture.

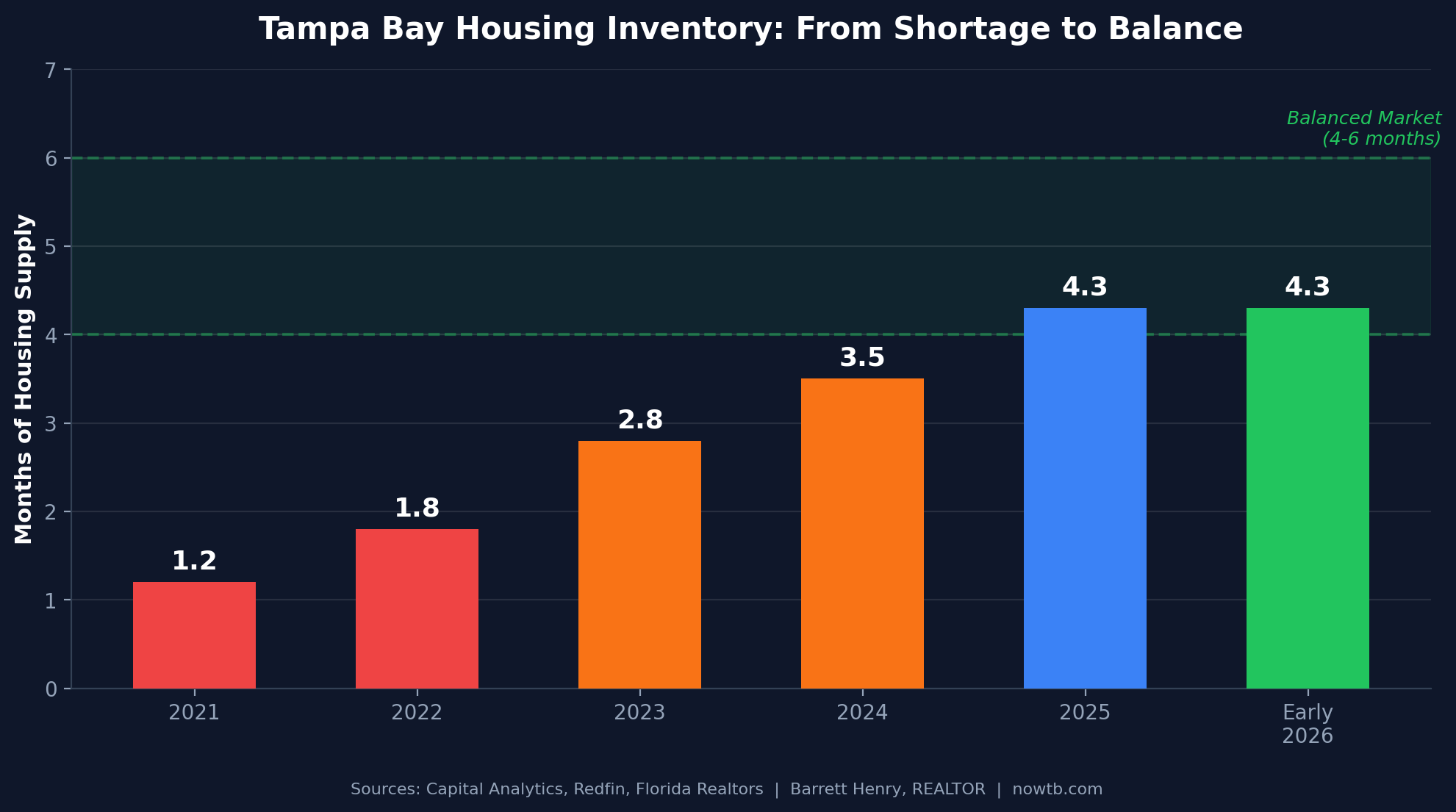

Supply Is Growing, and That’s Healthy

Tampa Bay inventory has increased meaningfully. The Home Buying Institute reported that active listings in the Tampa Bay area rose about 14.8% year-over-year heading into 2026. Redfin’s data showed the Tampa metro at approximately 5.4 months of housing supply, well above the national average of 3.8 months. Other sources like Capital Analytics Associates and Moving to Florida Guide peg Tampa Bay supply closer to 4 to 4.3 months.

Either way, the point is the same: we’ve moved from the artificially tight conditions of 2021 through 2023 into something much more normal. Buyers have choices. Sellers face real competition for attention. And that’s exactly how a healthy market is supposed to work.

Prices Are Stabilizing, Not Crashing

This is the part people get confused about. Redfin’s January 2026 data shows Tampa’s median sale price at $448K, up 9.1% year-over-year. But the broader metro area (which includes more suburban and affordable corridors) tells a more nuanced story. Zillow’s metro-wide data showed the average home value at approximately $354,666 as of late 2025, reflecting some softening from peak levels.

What does that mean? It depends on your ZIP code, price band, and property condition. Certain neighborhoods are appreciating. Others have pulled back from peak pricing. Overpriced listings are sitting. Well-priced, well-presented homes are still attracting solid activity.

This is a market that rewards precision. It punishes lazy pricing.

How Different Tampa Submarkets Are Behaving

Tampa Bay is not one market. It’s dozens of micro-markets that move at different speeds.

Valrico, Brandon, Riverview, and FishHawk/Lithia: Family-driven demand is active. School zones matter. Move-in ready homes that are priced to the most recent comps (not last year’s comps) are getting showings in the first week. Buyers are negotiating repairs and credits, which is normal and healthy.

South Tampa and St. Pete: Lifestyle-driven pockets with constrained land. Values tend to hold better because supply stays tight and demand is resilient. But even here, overpricing gets punished.

New construction corridors (south Hillsborough, Wimauma, parts of Pasco): Builder incentives are aggressive. Rate buydowns, price reductions, and closing cost packages are common. Resale sellers in these areas are competing directly with new-home incentives, which puts extra pressure on pricing.

Condo markets: More challenging. Insurance costs, HOA increases, and special assessments (especially post-Surfside legislation) are keeping some buyers cautious. Condo inventory is growing faster than single-family.

This Is Not 2008. Not Even Close.

Every time rates move or headlines get negative, people ask the same question.

It’s not 2008. Two facts make that clear.

Credit quality is dramatically stronger. Today’s borrowers go through far stricter underwriting than pre-2008. The Urban Institute’s Housing Finance Chartbook has reported median agency credit scores around 748 in recent tracking periods. That’s not a loose-credit bubble.

Homeowners have massive equity and foreclosures are a fraction of crisis levels. CoreLogic (now Cotality) reported total U.S. net homeowner equity exceeding $17.5 trillion. And while foreclosure activity has ticked up, ATTOM Data reported roughly 289,000 foreclosure starts in 2026, compared to over 2.1 million at the 2009 peak. That’s a completely different universe.

Most owners hold fixed-rate mortgages at rates well below today’s levels. They’re not forced sellers. There’s no systemic pressure creating a wave of distressed inventory.

What I’m Seeing From My Desk (Barrett’s Real-Time Perspective)

Here’s what’s actually happening in my day-to-day across Tampa Bay:

Serious buyers are writing offers again. But they’re more analytical than the 2021 crowd. They’re running comps, asking about insurance costs, and comparing total monthly costs, not just purchase price.

Well-priced homes still attract strong early activity, especially in school-driven neighborhoods with newer roofs and updated kitchens/baths. The first 7 to 10 days on market still matter the most.

Negotiation is back. I’m seeing more seller credits, repair requests, and closing cost assistance than at any point in the last four years. Buyers who are prepared and pre-approved have genuine leverage.

Overpricing gets punished fast. With more inventory and more data-savvy buyers, a listing priced above the comps will sit. And once it sits past 30 days, the perception shifts. I’d rather price it right on day one than chase the market with reductions.

Insurance is a real factor in every deal. Buyers are asking about insurance costs before they even schedule a showing. Homes with newer roofs, updated electrical, and no prior claims are getting a pricing premium because they’re cheaper to insure.

Why Buyers Should Be Acting Now

This is a rare window where multiple factors line up in the buyer’s favor at the same time.

Rates are the lowest in over three years. The 30-year fixed is sitting around 5.87% (Zillow) and Freddie Mac’s weekly average just hit 6.01%.

Inventory is meaningfully higher than the past several years. More homes to see, more time to decide, less pressure to waive contingencies.

Sellers are offering concessions. Rate buydowns, closing cost credits, and repair allowances are back on the table.

Competition is lower than it will be. If rates continue dropping, pent-up demand floods back in. The National Association of REALTORS® has estimated that a 1% rate decrease can bring roughly 5.5 million additional households into the pool of potential buyers.

The smart buyer strategy: buy now while you have leverage, lock in today’s rates, and if rates drop further, refinance later. Waiting for the “perfect” rate often means competing with everyone else who was also waiting.

Why Sellers Should Be Encouraged

If you’re thinking about selling, the environment is better than the headlines suggest.

Improving rates are expanding the buyer pool. Every time rates drop, more buyers qualify. More qualified buyers means more potential offers on your home.

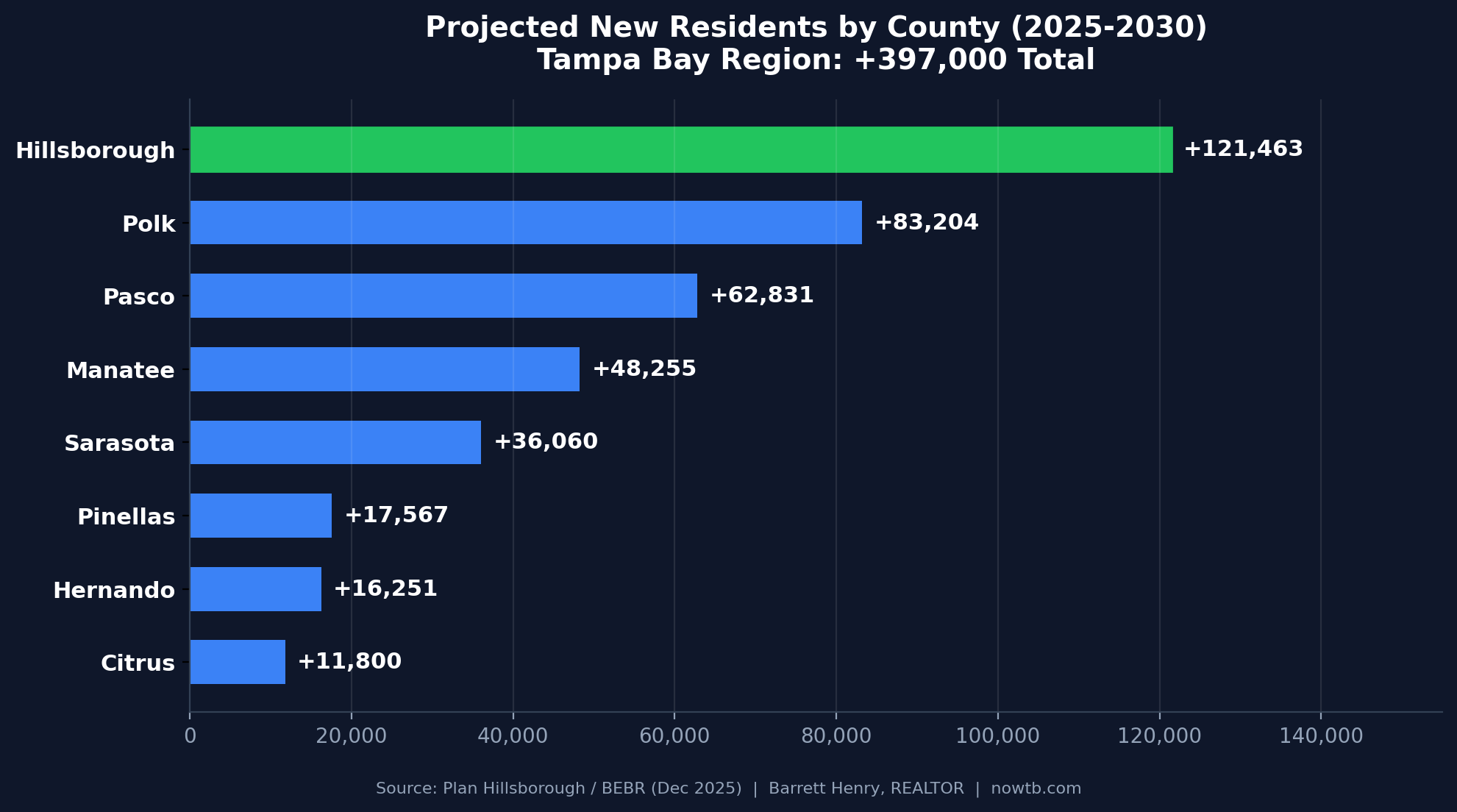

Tampa Bay demand is structurally supported. The region continues to attract new residents. Plan Hillsborough’s analysis of BEBR projections shows the Tampa Bay region (eight counties) adding approximately 397,000 new residents by 2030, with Hillsborough County alone projected to gain over 121,000.

Well-executed listings are still winning. This is a market where strategy matters. Pricing to the most recent comps, professional photography, and a strong first-week marketing push can generate strong results.

What’s changed: you can’t overprice by $30K and expect multiple offers in 48 hours. That market is gone. What works now is disciplined pricing, sharp presentation, and proactive negotiation.

The Bigger Economic Picture Supporting Housing

Real estate doesn’t exist in a vacuum. The broader economy either supports or undermines housing activity. Right now, it’s doing the former.

Inflation is trending down. That’s what allowed the Fed to cut rates three times in late 2025 and what’s keeping mortgage rates on a downward trajectory. The Fed held steady in January 2026 and isn’t meeting again until mid-March, which means the current rate environment has room to hold.

The job market remains resilient. Tampa Bay led Florida in job growth across several sectors in 2026 according to CoStar reporting. Healthcare, finance, defense, and logistics continue to anchor the regional economy. A stable job market supports buyer confidence and mortgage qualification.

Homeowner equity is at record levels. CoreLogic (now Cotality) reported total U.S. net homeowner equity exceeding $17.5 trillion. That means most homeowners are in strong financial positions, not forced sellers. That equity cushion keeps distressed inventory low and supports price stability.

Refinance activity is surging. Freddie Mac noted that refinance application activity has more than doubled over the past year, with many recent buyers reducing their annual mortgage payments by thousands of dollars.

The Long-Term Case for Tampa Bay Real Estate

Population growth is projected to continue at pace. Plan Hillsborough’s analysis of BEBR projections shows the Tampa Bay region (eight counties: Hillsborough, Pinellas, Pasco, Polk, Manatee, Sarasota, Citrus, and Hernando) adding approximately 397,000 new residents by 2030. Under a momentum scenario, that number could reach 548,000. Hillsborough County alone is projected to gain over 121,000 new residents by 2030.

Since 2020, over 270,000 new residents have already chosen Tampa Bay. Migration from states like New York, New Jersey, Illinois, and California continues, driven by lifestyle, affordability relative to origin markets, no state income tax, and remote work flexibility.

Florida’s population engine shows no signs of slowing. The state is projected to gain roughly 306,000 net new residents annually through 2030 according to the state’s Demographic Estimating Conference. That’s approximately 838 new residents every day.

Tampa Bay’s economic base is diversified. Unlike single-industry markets that collapse when one sector struggles, Tampa Bay’s economy spans healthcare, financial services, defense (MacDill AFB), technology, logistics, tourism, and professional services. That diversity creates employment stability that supports housing demand.

No state income tax remains a permanent draw. For high-income relocators from states with 5% to 13%+ income taxes, the savings alone can justify a move. This is a structural advantage that isn’t going away.

The Insurance Factor That Changes Every Deal

No honest conversation about Tampa Bay real estate in 2026 is complete without talking about insurance.

Florida homeowners insurance has been one of the biggest headaches in the market. Premiums have risen sharply over the past several years. Some insurers left the state entirely. Others dramatically increased rates.

The impact on real estate is direct. Buyers now factor insurance costs into their purchase decision at the very beginning of the process, not as an afterthought at closing. A home with a newer roof (within the last 5 to 7 years), no prior claims, and a location outside major flood zones will be significantly cheaper to insure than an older home in a coastal or flood-prone area.

What this means for buyers: get an insurance quote before you write an offer. Not after. The difference between $2,500/year and $7,000/year changes your total monthly cost by $375. That’s as impactful as a full percentage point on your mortgage rate.

What this means for sellers: if your roof is aging, addressing it before listing can dramatically improve your home’s marketability. Buyers aren’t just looking at your kitchen counters. They’re looking at your roof age, your four-point inspection report, and your claims history.

Rate Forecasts: What the Experts Are Saying

Fannie Mae (updated February 12, 2026): Projects the 30-year rate averaging near 6% through 2026, with a path toward approximately 5.9% by year-end.

Mortgage Bankers Association (updated January 21, 2026): Expects the 30-year rate near 6.10% through most of 2026, with rates remaining in a similar range into 2027 (6.20% to 6.30%).

What both agree on: Rates are unlikely to return to the 2% to 3% pandemic levels. The high-5% to low-6% range is the new baseline.

What it means for you: Don’t base your entire housing decision on a rate forecast. Rates could go lower, stay flat, or tick back up depending on inflation data, Fed policy, and global events. This is a materially better rate environment than 2023 or 2024, and it’s unlikely to get dramatically worse in the near term.

The Refinance Opportunity for Current Homeowners

This article focuses on buyers and sellers, but there’s a third group benefiting from the rate drop: current homeowners who bought in 2023 or 2024 at higher rates.

Freddie Mac reported that refinance application activity has more than doubled over the past year. If you locked in a rate at 7% or higher, today’s environment near 5.87% to 6.01% could represent a meaningful reduction in your monthly payment.

A simple calculation: on a $400,000 loan, dropping from 7% to 5.87% saves approximately $305/month or $3,660/year. Even if you bought recently, talk to your lender about whether a refinance makes sense. Factor in closing costs (typically 2% to 3% of the loan balance) and calculate your break-even point. If you plan to stay in the home for more than 2 to 3 years, the math often works in your favor.

Frequently Asked Questions

Will Tampa Bay home prices drop in 2026?

The market is stabilizing, not collapsing. Some neighborhoods may see modest softening from peak prices, while others — especially supply-constrained lifestyle areas — are holding steady or appreciating. It depends heavily on your specific location, price point, and property condition. Broad predictions about “the Tampa Bay market” miss the reality that every micro-market behaves differently.

Should I wait for mortgage rates to drop below 5%?

Most forecasts do not project sub-5% rates becoming common anytime soon. Fannie Mae and the MBA both see rates hovering around 6% through 2026, with possible dips into the high 5s. If the payment works and the home is right, acting now preserves your negotiating leverage before competition increases. You can always refinance later if rates drop further.

Is a 6% mortgage rate good or bad?

Historically, 6% is completely normal. The 2% to 3% pandemic rates were the anomaly, made possible by unprecedented government intervention. Looking at the full history tracked by Freddie Mac since 1971, rates spent decades above 6%, including stretches above 10% and even 18% in the early 1980s. A 6% rate with today’s inventory and negotiating leverage is a better buying environment than 3% rates with 20 competing offers.

Is Tampa Bay still a good place to buy real estate long-term?

Population growth projections, job market diversity, no state income tax, and lifestyle appeal all support the long-term case. But “good investment” still depends on the specific property: its location, insurance profile, flood zone status, condition, and your purchase price. Tampa Bay as a region has strong fundamentals — that does not mean every property at every price is a good deal.

Is it better to buy a house now or wait until 2027?

The math depends on your situation, not the calendar. Current conditions offer a rare combination: rates at a three-year low, elevated inventory giving buyers real options, and sellers who are more willing to negotiate than they have been in years. Waiting assumes prices will drop enough to offset the cost of continued renting and the risk that rates rise again. For most Tampa Bay buyers, the right property at today’s terms beats hoping for a theoretical better deal later.

Can I refinance later if mortgage rates drop more?

Yes, and this is one of the strongest arguments for buying now. A purchase locks in today’s price and today’s terms. If rates drop a full percentage point or more in the future, refinancing typically costs $3,000 to $6,000 in closing costs and can be done without moving or renegotiating. You cannot go back in time to buy at today’s prices if they appreciate while you wait for lower rates.

What is the biggest mistake Tampa Bay buyers and sellers make right now?

Using outdated expectations. Buyers expecting 2021 competition or 2012 pricing. Sellers expecting 2021 pricing with 2026 inventory. The market rewards people who deal with current reality, not nostalgia. Working with an agent who reads the data and adjusts strategy accordingly — rather than one who tells you what you want to hear — makes a measurable difference in outcomes.

Final Thoughts

Right now, the data says: rates are the best in three years, inventory is healthier than it’s been since pre-pandemic, buyers have genuine negotiating power, and Tampa Bay’s long-term demand drivers remain intact.

That’s not a bad market. That’s an opportunity market.

Whether you’re buying, selling, investing, or relocating, the question isn’t “is the market good or bad?” The question is: “what’s the right strategy for my situation in today’s conditions?”

That’s the conversation I have with every client. And it’s one I’m happy to have with you.

Sources: Freddie Mac PMMS (Feb 19, 2026), Zillow Daily Mortgage Rates (Feb 24, 2026), CBS News, Yahoo Finance, Home Buying Institute, Redfin, Capital Analytics Associates, Moving to Florida Guide, Cameron Academy, Plan Hillsborough/BEBR Population Projections, ATTOM Data, CoreLogic/Cotality, Urban Institute, National Association of REALTORS®, Mortgage Reports.

Related Articles

Explore Tampa Bay Communities

Helpful Resources

About Barrett Henry — Barrett Henry is a licensed real estate Broker Associate with REMAX Collective, specializing in the Brandon, Riverview, Valrico, and greater Tampa Bay markets. With deep local knowledge and an honest, data-driven approach, Barrett helps buyers and sellers make confident real estate decisions. Learn more

Disclosure: This article is for informational purposes only and does not constitute financial or legal advice. Loan program details, rates, and limits change regularly — verify all information with a licensed mortgage lender before making decisions. Barrett Henry is a licensed real estate broker, not a mortgage lender.

Last Updated: February 23, 2026

Need Help With Tampa Bay Real Estate?

Barrett Henry is a licensed Broker Associate with REMAX Collective, serving the entire Tampa Bay market. Whether you are buying, selling, or investing — get straight talk and real data. No pressure, no games.

Schedule a Free Consultation Call (813) 733-7907