Quick Answer

What is the current state of the Apollo Beach real estate market after Hurricanes Helene and Milton?

Apollo Beach is in a post-hurricane correction with waterfront home prices down 5-12% from pre-storm levels. Back-to-back hurricanes in late 2024 created a buyer’s market with elevated inventory, motivated sellers, and generous concessions. Non-waterfront communities like Waterset remain stable with only 1-3% declines. For long-term buyers who can handle higher insurance costs, this is one of the best buying windows in years. Search Apollo Beach homes for sale.

The Apollo Beach real estate market is in a moment unlike anything I’ve seen in my years working south Hillsborough County. Back-to-back hurricanes – Helene in late September 2024 and Milton in October 2024 – rattled this waterfront community in ways that are still playing out across the MLS, the insurance market, and the psychology of buyers and sellers. Some homeowners are leaving. Some investors are arriving. Some properties are selling at deep discounts, and others are holding firm. I’m Barrett Henry with REMAX Collective, and I’m going to give you the honest, ground-level picture of what’s happening in Apollo Beach right now – the challenges, the opportunities, and what the data actually says. If you’re thinking about buying, selling, or investing in Apollo Beach in 2026, this is the analysis you need before making a move.

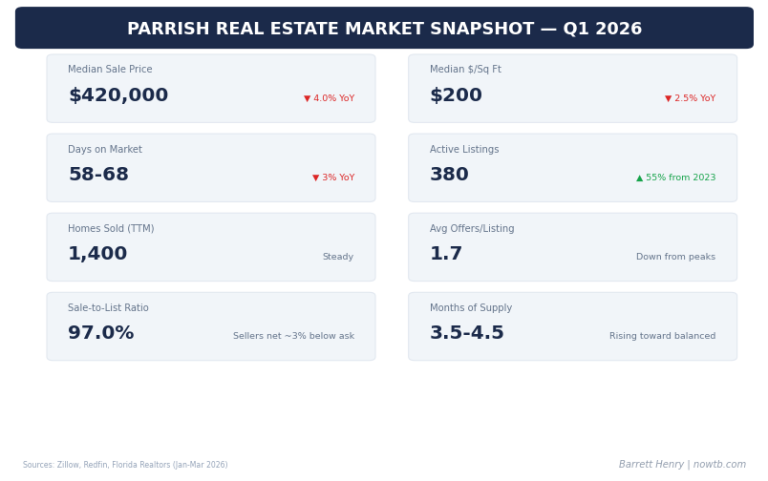

Apollo Beach Market Snapshot – January 2025

| Market Metric | Apollo Beach (33572) | Trend vs. Last Year |

|---|---|---|

| Median Home Price (all types) | $385,000–$420,000 | Down 3–6% year-over-year |

| Median Price Per Square Foot | $210–$240 | Down 4–7% |

| Average Days on Market | 55–75 days | Up from 35–45 days pre-hurricanes |

| Active Inventory | 180–220 listings | Up 40–55% from early 2024 |

| Months of Inventory | 5–6 months | Approaching buyer’s market territory |

| List-to-Sale Price Ration | 93%–96% | Down from 97%–99% pre-storms |

| Cash Buyer Percentage | ~35–40% | Up from ~25% pre-storms |

| Price Change YoY (waterfront) | Down 8–12% | Steepest declines in damaged properties |

| Price Change YoY (non-waterfront) | Down 1–3% | Inland communities more stable |

Apollo Beach Market Overview – The Post-Hurricane Reality

Let me be direct about where things stand. Apollo Beach took real damage from both storms. Hurricane Helene brought significant storm surge to canal-front and bayfront properties in late September 2024, and before many homeowners could finish cleanup, Hurricane Milton hit in early October with high winds and additional flooding. The one-two punch was devastating for some areas – particularly the original canal neighborhoods along Apollo Beach Boulevard South, parts of Symphony Isles, and lower-elevation bayfront properties near MiraBay’s waterfront sections.

Not every home was damaged. Not every neighborhood was equally affected. Communities like Waterset, which sits inland and at higher elevation, came through with minimal issues. MiraBay’s newer construction fared better than older canal homes with lower floor elevations. But the cumulative effect on the market has been real: more inventory, more motivated sellers, longer days on market, and a pricing correction that’s concentrated in waterfront properties.

Here’s what I’m telling my clients: this is both a challenging and genuinely opportunistic market. The challenge is uncertainty – insurance, repair costs, and buyer confidence are all in flux. The opportunity is that waterfront properties in Apollo Beach are available at price points we haven’t seen since 2021, and for the right buyer with the right strategy, that window won’t stay open indefinitely.

Pre-Hurricane Market Trends: 2021–2024

To understand where Apollo Beach is now, you need to see where it was. The market here followed the same trajectory as the broader Tampa Bay housing market, but with the amplified volatility that waterfront communities tend to experience.

- 2021 – The frenzy: Apollo Beach waterfront homes appreciated 20–30%. Canal homes that were $300K in 2020 were selling for $380K–$420K. Bidding wars were common, especially for properties with deep-water docks and direct bay access. MiraBay homes routinely sold above asking.

- 2022 – Peak pricing: Median prices in 33572 hit all-time highs. Waterfront canal homes peaked in the $450K–$550K range. Non-waterfront homes in Waterset and Andalucia hit $350K–$420K. Then rates spiked mid-year and the momentum stalled.

- 2023 – Correction and stagnation: Days on market stretched. Some waterfront properties saw 5–8% price declines from their 2022 peaks. Inventory began building. Insurance cost increases started making headlines and affecting buyer calculations.

- Early 2024 – Stabilization: The market found a floor. Modest appreciation returned in some segments. MiraBay held value better than older canal homes. Waterset continued performing well with new construction attracting buyers who wanted lower insurance risk.

- Late 2024 – Hurricanes Helene and Milton: Everything changed. The market bifurcated sharply between damaged and undamaged properties, and between sellers who needed to get out and those who could wait.

How Helene and Milton Changed the Apollo Beach Market

The back-to-back hurricanes created a set of market dynamics that I haven’t seen before in this area. Here’s what happened and what’s still playing out.

Increased Inventory from Motivated Sellers

Within weeks of the storms, new listings in the 33572 zip code spiked. Some of these sellers had damaged homes they didn’t want to repair. Others had undamaged homes but decided the hurricane experience was the last straw – they’d been thinking about leaving Florida, and the storms pushed them over the edge. Still others faced insurance claim disputes or coverage gaps that made holding the property financially painful. The result: active inventory in Apollo Beach jumped 40–55% compared to the same period the year before.

Damaged Properties Hitting the Market As-Is

A significant number of homes are listed “as-is” with storm damage disclosed. These range from homes with minor cosmetic water damage to properties that need full gut renovations – drywall stripped to the studs, HVAC systems replaced, kitchens and bathrooms rebuilt. These as-is properties are selling at steep discounts – 15–30% below what a comparable undamaged home would command. For the right buyer (typically investors or experienced renovators), these represent real value. For the average homebuyer, they’re high-risk purchases that require careful due diligence.

Seller Motivation Is Higher Than Usual

I’m seeing more price reductions, more seller-paid closing cost credits, and more willingness to negotiate than at any point in the past four years. Sellers who are relocating out of the area or out of state are particularly motivated. Some are accepting offers 8–12% below their initial list price. This creates real opportunities for buyers who are willing to buy in a market that most people are afraid of.

Current Pricing Trends – Waterfront vs. Non-Waterfront

The hurricanes created a two-track market in Apollo Beach. Waterfront properties – especially older canal homes that took storm surge – are experiencing the steepest price declines. Non-waterfront properties in newer communities like Waterset are holding value much better.

Pricing by Property Type – January 2025

| Property Type | Price Range (Jan 2025) | Change from Pre-Hurricane | Notes |

|---|---|---|---|

| Waterfront canal home (undamaged) | $380,000–$520,000 | Down 5–8% | Strongest demand among waterfront buyers |

| Waterfront bayfront home (undamaged) | $500,000–$750,000+ | Down 5–10% | MiraBay bayfront holding best |

| MiraBay (non-waterfront) | $380,000–$480,000 | Down 2–4% | Amenity package supports value |

| Waterset | $350,000–$450,000 | Flat to down 2% | Inland location, newer build = stability |

| Non-waterfront (Andalucia, Mirabella) | $320,000–$400,000 | Down 1–3% | Minimal storm impact |

| Damaged / as-is canal homes | $200,000–$350,000 | Down 20–30% | Investor-dominated segment |

| Damaged / as-is non-waterfront | $220,000–$310,000 | Down 15–20% | Less inventory than waterfront damage |

The key takeaway: if you’re a buyer who wants waterfront in Apollo Beach and the property is undamaged with a clean inspection, you’re getting a 5–10% discount compared to what you’d have paid in early 2024. That’s meaningful – on a $450,000 canal home, that’s $22,000–$45,000 in savings. And sellers are more willing to negotiate closing costs and repairs on top of the reduced price.

Insurance Impact on the Apollo Beach Market

Insurance is the elephant in the room for every waterfront market in Florida, and in Apollo Beach it’s become the single biggest factor driving both buyer hesitation and seller motivation. Let me break down what’s actually happening.

Homeowners Insurance

Florida’s homeowners insurance market was already in crisis before the hurricanes. Carriers had been leaving the state, premiums were rising 20–40% per year, and many homeowners were being pushed to Citizens Property Insurance – Florida’s insurer of last resort. After Helene and Milton, the situation in Apollo Beach has intensified. Homeowners who filed claims are seeing non-renewals or premium increases that make their properties significantly more expensive to carry. New buyers are finding that insurance quotes for waterfront Apollo Beach homes can run $4,000–$8,000+ per year for wind/homeowners coverage alone – before flood insurance.

Flood Insurance and FEMA Risk Rating 2.0

FEMA’s Risk Rating 2.0 methodology, which calculates flood insurance premiums based on individual property risk rather than broad flood zone maps, has hit Apollo Beach particularly hard. Properties on canals and near the bay are seeing flood insurance premiums of $2,500–$6,000+ per year. Some bayfront properties are above $8,000. Combined with homeowners insurance, total insurance costs on a waterfront Apollo Beach home can exceed $10,000–$14,000 per year. That’s $830–$1,170 per month added to your housing cost – and it’s a number that makes some buyers walk away entirely.

I always tell my clients to get insurance quotes before you fall in love with a property. The purchase price might be attractive, but if insurance adds $12,000/year to your carrying costs, the total cost of ownership changes dramatically. For a deeper dive into Florida flood zones and what they mean for your wallet, read my full guide.

Investor Activity in Apollo Beach

Cash buyers and investors are more active in Apollo Beach right now than at any point I can recall. The numbers tell the story: cash transactions are running 35–40% of all sales in the 33572 zip code, up from about 25% before the storms. Here’s what’s driving that.

- Fix-and-flip investors are buying damaged canal homes at $200K–$350K, renovating them for $50K–$120K, and reselling in the $400K–$520K range. The margins work when you’re buying damaged properties at 20–30% discounts.

- Buy-and-hold investors are acquiring waterfront rental properties at post-hurricane prices, betting on long-term appreciation and short-term rental income. Apollo Beach canal homes rent well – the waterfront lifestyle attracts tenants willing to pay $2,500–$3,500/month.

- Out-of-state investors are coming in from markets like New York, New Jersey, and California, attracted by the price declines and Florida’s no-income-tax advantage. They see the hurricane discount as a buying opportunity, not a red flag.

- Insurance-savvy investors are buying older homes, completing full renovations to current building codes, and then securing insurance at rates that would be impossible on the original structure. A gut renovation with a new roof, impact windows, and updated electrical/plumbing can reduce insurance premiums by 30–50%.

Should this concern regular buyers? Not necessarily. Investor activity is actually a sign of confidence in the market’s long-term fundamentals. But it does mean that well-priced damaged properties are getting scooped up quickly – if you’re competing in that segment, you need to be ready to move fast with cash or a strong pre-approval. For more on investment property strategies in Tampa Bay, see my guide.

Buyer Opportunities in the Current Market

If you’re a buyer considering Apollo Beach right now, here’s where the opportunities are real.

- Undamaged waterfront at a discount: The best opportunity in Apollo Beach right now is buying a clean, undamaged canal or bayfront home at 5–10% below what it would have cost 12 months ago. These sellers are motivated by the market sentiment, not by damage – and you’re getting the same home for less money.

- Seller concessions are generous: Closing cost credits of $10,000–$20,000, rate buydowns, and home warranty inclusions are all on the table. I’m negotiating these into almost every deal right now.

- Less competition: Many buyers are sitting on the sidelines, scared by the hurricane headlines. That means less competition for the properties that are on the market. If you’re ready to buy, you’re competing against fewer people.

- Renovation opportunities: If you have the budget and risk tolerance, buying a damaged property and renovating it to current code gives you a home that’s more resilient, more insurable, and worth significantly more than what you paid. Not for everyone – but for the right buyer, the math is compelling.

- Inland Apollo Beach at near-normal pricing: Waterset and other non-waterfront communities are barely affected. If you want the 33572 zip code without the waterfront risk premium, these communities are stable and performing well.

If you’re a first-time buyer, I’d generally steer you toward the inland communities unless you have a strong cash position and are comfortable with the insurance costs. The waterfront deals are real, but they require eyes-wide-open financial planning.

Seller Strategies in the Current Market

If you’re selling in Apollo Beach right now, I’m going to be honest: it’s a tougher market than it was 18 months ago. But homes are still selling, and there are clear strategies that separate successful listings from the ones that sit.

- Price to the current market, not 2022: The biggest mistake I see sellers make is pricing based on what their neighbor’s home sold for two years ago. That market is gone. Price your home based on current comps – including the post-hurricane inventory – and you’ll attract serious buyers.

- Complete repairs before listing: If your home had storm damage and you’ve repaired it, get documentation. Buyers want to see the receipts, the permits, and the inspections. A fully repaired home with documentation sells faster and for more money than one with lingering questions about damage.

- Offer insurance documentation: If you have a current, assumable insurance policy or can provide recent premium quotes, share that with buyers. Insurance uncertainty is killing deals in Apollo Beach right now. Removing that uncertainty is a competitive advantage.

- Be prepared to negotiate: Budget for closing cost credits, home warranty coverage, and potential repair requests. The sellers who build these costs into their pricing strategy from day one end up netting more than those who resist and watch their listing sit for 90+ days.

- Consider the timing: Spring 2025 will bring more buyers into the market. If you can wait until February–April to list, you’ll likely face more demand. But if you need to sell now, price it aggressively and make it easy for buyers to say yes.

For a more detailed guide on selling strategy, see my guide to selling your home in the Tampa Bay area.

Apollo Beach vs. Other Waterfront Markets

If you’re looking at waterfront property in the Tampa Bay area, Apollo Beach isn’t your only option. Here’s how it compares to other markets I work regularly.

| Factor | Apollo Beach | South Tampa | Ruskin | St. Petersburg |

|---|---|---|---|---|

| Median waterfront price | $400K–$550K | $700K–$1.2M+ | $300K–$450K | $550K–$900K+ |

| Hurricane impact (2024) | Moderate to severe | Moderate (surge areas) | Moderate | Moderate (coastal) |

| Insurance costs | $8K–$14K/yr (waterfront) | $6K–$12K/yr | $6K–$10K/yr | $5K–$10K/yr |

| Inventory level | Elevated (buyer’s market) | Moderate | Elevated | Moderate |

| Bay/Gulf access | Canal system to Tampa Bay | Direct bay/Hillsborough River | Bay and river access | Direct bay/Gulf |

| Community feel | Coastal suburb, laid-back | Urban, walkable, upscale | Rural transitioning, affordable | Urban, arts/dining scene |

| Post-hurricane opportunity | Strongest discounts | Moderate discounts | Good discounts | Selective discounts |

| Best for | Boaters, value-seekers, investors | Urban waterfront lifestyle | Budget waterfront buyers | Lifestyle + appreciation |

Apollo Beach stands out for one specific reason: it offers the deepest post-hurricane discounts on waterfront property with direct bay access in the Tampa Bay metro. If you’re a buyer with tolerance for the insurance complexity and a long-term investment horizon, the value proposition right now is arguably the strongest of any waterfront submarket in the area. For a broader look at the waterfront homes market across Tampa Bay, see my full guide.

Apollo Beach Market Forecast – 2025

I don’t do hype and I don’t do doom. Here’s my honest, data-informed outlook for the Apollo Beach real estate market in 2026.

What I Expect

- Waterfront prices will stabilize by mid-2025: The initial post-hurricane selling wave is already winding down. By Q2 2025, the most motivated sellers will have already sold, and the remaining inventory will be priced more rationally. I expect waterfront prices to find a floor 5–10% below pre-hurricane levels and then begin slowly recovering.

- Non-waterfront properties will recover faster: Waterset, Andalucia, and Mirabella barely felt the hurricane impact on pricing. These communities will likely see flat to modest 2–3% appreciation through 2025 as confidence returns.

- Insurance will remain the wildcard: If the Florida legislature passes meaningful insurance reform and premiums stabilize, buyer confidence in waterfront Apollo Beach will improve significantly. If premiums keep rising 15–20% per year, it will continue to suppress demand and prices for waterfront properties.

- Investor activity will peak in Q1–Q2 2025: The window for the deepest discounts on damaged properties is closing. Most fixable damaged inventory will be absorbed by investors in the first half of the year.

- Spring 2025 will bring more traditional buyers: As the storm season recedes in memory and more buyers see the discounted pricing, I expect increased buyer activity from people who genuinely want to live in Apollo Beach – not just flip properties. This will support prices in the undamaged segment.

- No crash, no V-shaped recovery: Apollo Beach won’t return to 2022 peak prices anytime soon, but it also isn’t going to collapse further. This is a market that’s repricing to account for real risks (hurricanes, insurance costs) while maintaining the fundamental appeal (waterfront living, bay access, lifestyle) that has always driven demand here.

Pros and Cons of Buying in Apollo Beach Right Now

Pros

- ✓ Waterfront prices at 2021 levels – Canal and bayfront homes available at prices not seen in 3+ years. Genuine discount opportunity for long-term buyers.

- ✓ Motivated sellers and generous concessions – Closing cost credits, rate buydowns, and repair credits are widely available. Buyers have negotiating leverage.

- ✓ Less competition from other buyers – Fear is keeping many buyers away. If you’re willing to buy when others won’t, you’ll get better deals.

- ✓ Bay access and boating lifestyle at a fraction of South Tampa prices – The lifestyle hasn’t changed. The water, the canals, the manatees, the sunsets – all still there.

- ✓ Renovation opportunities with major upside – Buy damaged, renovate to current code, and own a more resilient home worth significantly more than your total investment.

- ✓ Inland communities barely affected – Waterset and other non-waterfront neighborhoods offer stability, newer construction, and lower insurance costs within the same zip code.

- ✓ Long-term fundamentals intact – Tampa Bay population growth, Florida’s tax advantages, and the limited supply of waterfront land all support long-term appreciation.

Cons

- ✗ Insurance costs are punishing – Total insurance on a waterfront home can exceed $10,000–$14,000/year. This is the single biggest financial headwind for Apollo Beach buyers.

- ✗ Hurricane risk is real and proven – Helene and Milton weren’t hypothetical. The damage happened. Future storms will too. You must be prepared financially and emotionally.

- ✗ Uncertainty about future insurance availability – Some carriers are pulling out of Florida coastal markets. If your current insurer non-renews, your replacement options may be limited and expensive.

- ✗ Damaged property purchases carry renovation risk – Hidden mold, structural damage, and code compliance issues can turn a “deal” into a money pit without proper inspections and contractor vetting.

- ✗ Resale uncertainty in the near term – If you need to sell within 2–3 years, you may not recoup your investment. This market favors long-term holders.

- ✗ Seawall and flood zone costs add up – Between seawall maintenance, flood insurance, and CDD fees in newer communities, the total cost of ownership can surprise buyers who focus only on the purchase price.

- ✗ Lender scrutiny is increasing – Some lenders are tightening requirements for flood zone properties, requiring higher down payments or additional documentation. Cash buyers face fewer obstacles.

Frequently Asked Questions About the Apollo Beach Real Estate Market

Is now a good time to buy in Apollo Beach?

It depends on your situation, risk tolerance, and timeline. If you’re a long-term buyer (5+ year hold) who wants waterfront living and can handle the insurance costs, this is one of the best buying windows in years. Prices are discounted, sellers are negotiating, and competition is low. If you need short-term liquidity or can’t absorb the insurance costs, it may not be the right time. I walk every client through the full financial picture before we write an offer.

How much did Apollo Beach home prices drop after the hurricanes?

Waterfront homes in Apollo Beach have declined roughly 5–12% from pre-hurricane levels, depending on the property type and condition. Damaged as-is properties have seen declines of 20–30%. Non-waterfront communities like Waterset are down only 1–3%. The declines are concentrated in older canal-front homes that took storm surge damage and properties where insurance complications are affecting the sale.

How much is flood insurance in Apollo Beach?

Flood insurance premiums in Apollo Beach vary widely based on the property’s specific risk profile under FEMA’s Risk Rating 2.0. For canal-front homes in AE flood zones, expect $2,500–$6,000+ per year. Bayfront properties in VE zones can exceed $8,000/year. Inland properties in Zone X may be as low as $500–$1,200/year. Elevation, distance to water, and the home’s first-floor height are the primary factors. Always get a flood insurance quote before making an offer on any Apollo Beach property.

Are investors buying up all the good deals in Apollo Beach?

Investors are very active in the damaged property segment, where cash offers dominate. However, in the undamaged waterfront and non-waterfront segments, traditional buyers are still competitive – especially with financing and reasonable contingencies. The best deals on damaged properties do tend to go to cash buyers who can close quickly, but there are still plenty of opportunities for financed buyers in the clean inventory. Working with an agent who knows the local inventory is key to finding the right property before investors do.

Should I buy a hurricane-damaged home in Apollo Beach?

Only if you have the financial resources, the patience for a renovation, and a trusted contractor who knows Florida building codes. The potential upside is real – buying at $250K, renovating for $80K–$120K, and owning a home worth $420K–$500K. But the risks are also real: hidden mold, structural issues, permit delays, and insurance complications. I recommend a thorough home inspection by an inspector experienced with storm damage, plus a detailed contractor estimate, before committing to any damaged property.

Will Apollo Beach home prices recover?

Yes, I believe they will – but it won’t happen overnight. The fundamental appeal of Apollo Beach – waterfront living with bay access in a growing metro area – hasn’t changed. What has changed is the market’s pricing of risk, particularly insurance and hurricane exposure. I expect prices to stabilize by mid-2025 and begin a gradual recovery over the following 2–3 years, assuming no major additional storm events. Homes that are renovated to current building codes with strong insurance profiles will recover fastest.

How do I get insurance for a waterfront home in Apollo Beach?

Start with an independent insurance agent who specializes in Florida coastal properties – not a national call center. You’ll likely need separate homeowners/wind and flood policies. Options include private market carriers, Citizens Property Insurance (Florida’s state-backed insurer of last resort), and private flood insurance alternatives to the NFIP. Newer homes with impact windows, hip roofs, and updated systems qualify for better rates. Homes with recent hurricane damage claims on record may face higher premiums or limited carrier options. Get quotes early in the buying process – before you’re emotionally committed to a property.

Sources

Data and market observations referenced in this guide come from the following sources (accessed January 2025):

- Stellar MLS (My Florida Regional MLS) – Active Listings, Sold Data, Days on Market, 33572 Zip Code

- Zillow Research – Home Value Index, Apollo Beach / Tampa Bay Metro

- Redfin Market Data – Apollo Beach Housing Market Overview

- Hillsborough County Property Appraiser – Sales Records and Assessed Values

- FEMA Flood Map Service Center – Flood Zone Designations, Apollo Beach

- FEMA Risk Rating 2.0 – Flood Insurance Premium Methodology

- Florida Office of Insurance Regulation – Property Insurance Market Reports

- National Hurricane Center – Hurricane Helene and Milton Impact Reports

- Citizens Property Insurance Corporation – Policy Data, Hillsborough County

- Freddie Mac – Primary Mortgage Market Survey, 30-Year Fixed Rates

Want a Real Assessment of Apollo Beach Right Now?

I’m not going to sugarcoat it or scare you. I’ll give you the honest numbers and help you decide if now is the right time to buy or sell in Apollo Beach. Every situation is different – let’s talk about yours.

Barrett Henry | REMAX Collective

Direct: (813) 733-7907

Email: [email protected]

Website: NOWtb.com

Call or text me anytime at (813) 733-7907. Whether you’re trying to figure out if a waterfront deal is legit, need help understanding the insurance math, or want to know what your Apollo Beach home is worth in today’s market – I’m here to help.

This market analysis was written by Barrett Henry, a licensed REMAX Collective real estate agent serving the Tampa Bay area. The information provided is based on local market knowledge, MLS data, and publicly available sources. Home prices, insurance rates, inventory levels, and market conditions are subject to change. This guide provides general market analysis and should not be considered financial or investment advice. Always verify current information and consult licensed professionals before making buying or selling decisions.

Related Guides

- Apollo Beach, FL Community Guide

- Selling a Hurricane-Damaged Home in Apollo Beach

- Apollo Beach Waterfront Homes Guide

- Tampa Bay Housing Market 2025

- Florida Homeowners Insurance Guide

- Florida Flood Zones Guide

- Waterfront Homes in Tampa Bay

- Investment Property in Tampa Bay

- First-Time Home Buyer Guide – Brandon FL

Last updated March 2026

Related Articles

Explore Tampa Bay Communities

About Barrett Henry – Barrett Henry is a licensed real estate Broker Associate with REMAX Collective, serving Apollo Beach and the Hillsborough County area. With deep local knowledge and an honest, data-driven approach, Barrett helps buyers and sellers make confident real estate decisions. Learn more

Disclosure: This article is for informational purposes only and does not constitute financial or legal advice. Market data is approximate and subject to change. Always consult with a qualified real estate agent, lender, or attorney for your specific situation.

Last Updated: March 2026

Need Help With Tampa Bay Real Estate?

Barrett Henry is a licensed Broker Associate with REMAX Collective, serving the entire Tampa Bay market. Whether you are buying, selling, or investing – get straight talk and real data. No pressure, no games.

Schedule a Free Consultation Call (813) 733-7907